- mssng

- Posts

- Who’s to blame for the Housing Crisis? Private Housebuilders

Who’s to blame for the Housing Crisis? Private Housebuilders

#5 Why has the private sector not built more?

mssng is on a mission to tackle tough questions and spark new insights through the power of data. Our blog dives into the heart of the issues — some of those big topics that fuel debate, make headlines, shape policies, or change behaviours. We go to the source, uncovering the data to bring you clear, meaningful context. We hope these insights make your inbox a little more interesting, and if you have a challenge that could use a data-driven edge, we’d love to hear from you.

The UK has a housing crisis, consistently failing to build enough new stock in line with government targets. Why hasn’t the private sector stepped in to meet the rise in market demand?

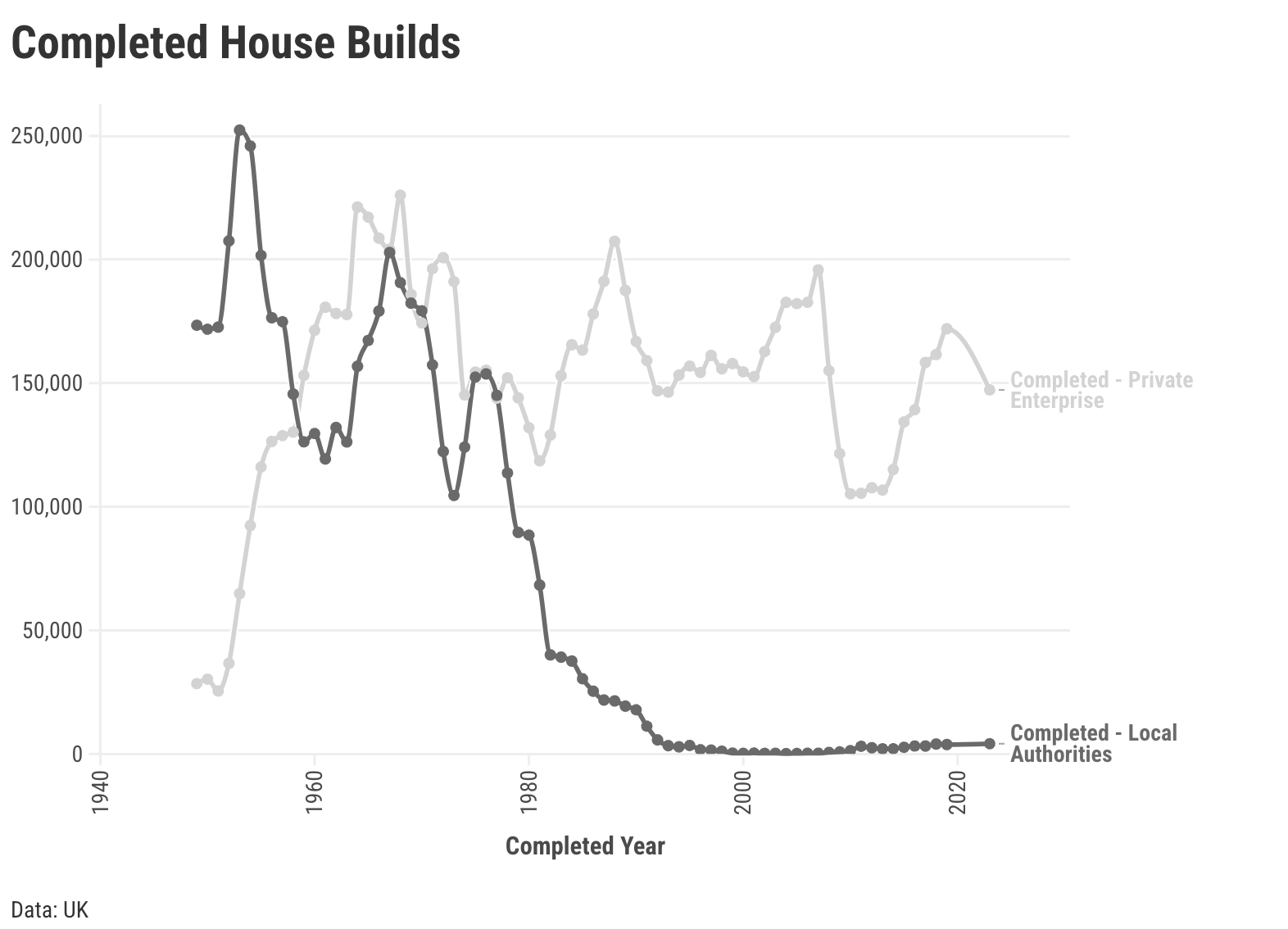

Before we go there, it’s worth a quick history lesson. There was a sustained period of building of new homes in the post-war years, not just to replace those dwellings that were lost, but also to support the creation of new industries in targeted areas of the country. It was initially driven by the public sector, with the private sector housebuilders taking a supporting role until the 1960s from when delivery output was roughly a 50:50 split.

Between 1946-1980, social housing accounted for an average 126,000 of the new dwellings built every year and by the end of that 35-year period, the idea of a housing shortage had been consigned to history.

Things changed with the the 1980 Housing Act and the Right to Buy policy of Margaret Thatcher’s Conservative government. This enabled tenants to buy their own council house or flat and achieve that dream of home ownership. A subsequent decision in 1981 then prevented local authorities using the revenue to build new housing stock, meaning the replacement rate of social housing quickly became a small fraction of the post-war building boom. Between Oct-Dec 1978, local authorities in England completed 24,200 new dwellings. In the three months of Oct-Dec 2023, it was just 760 [1].

By the early 2000s, the exceptionally high demand for homes, both to buy and to rent, had created a clear opportunity for the private sector to pick up the slack – so, why hasn’t that happened?

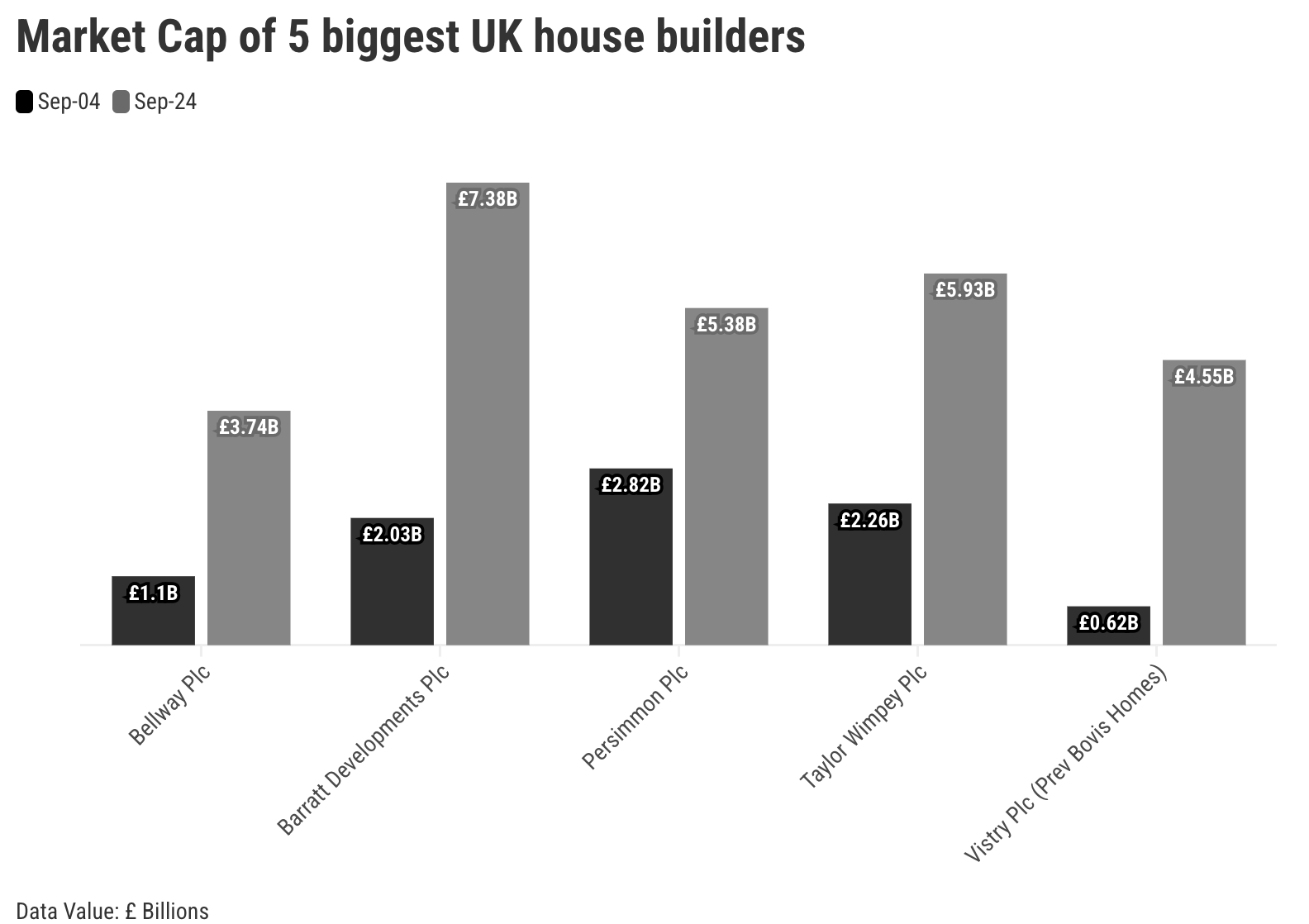

It’s certainly fair to say that the planning process has not helped and needs reforming (see post #4 on Planning). However, private housebuilders have still flourished even though the planning handbrake has been on. The market cap (that’s the cash value) of the five biggest housebuilders over the past 20 years has grown significantly, despite a financial crash in 2008 and the rising cost of building materials and labour.

source: MarketScreener / Google Finance / CompaniesMarketCap

In the recent past, bonuses paid to senior executives were making headlines for all the wrong reasons. The CEO of Persimmon was paid a staggering £75m bonus in 2018 at a time when the company profit margin was getting a huge boost from the taxpayer-funded ‘Help to Buy’ initiative [2].

The Competition & Markets Authority (CMA) reported in February 2024 that the profitability of the largest private housebuilders was found to be “generally higher than we would expect in a well-functioning market during those periods outside the Global Financial Crisis and its immediate aftermath. Profits in the period from 2013 to 2019 were particularly high” [3].

The CMA was tasked with investigating the sector for anti-competitive practices, and it also looked at the number of potential building plots that private housebuilders have been stockpiling (known as ‘land banking’). It estimated the top 11 private housebuilders had 1.17 million plots available for building [4], which is the equivalent to almost half the area of the Isle of Wight. Nevertheless, the CMA did not see the amount of land banking to be a significant factor in limiting the delivery of new homes - failures in the planning process were a much more significant cause.

mssng

The CMA report found that ‘build-out’ rates on residential sites were being paced in line with consumer demand to maintain high price levels [6]. However, while noting that this does slow the rate of housing delivery, the CMA concluded it was further evidence that the private sector has purely commercial motivations - it is not best equipped to help solve a wider housing need that has affordability at its heart.

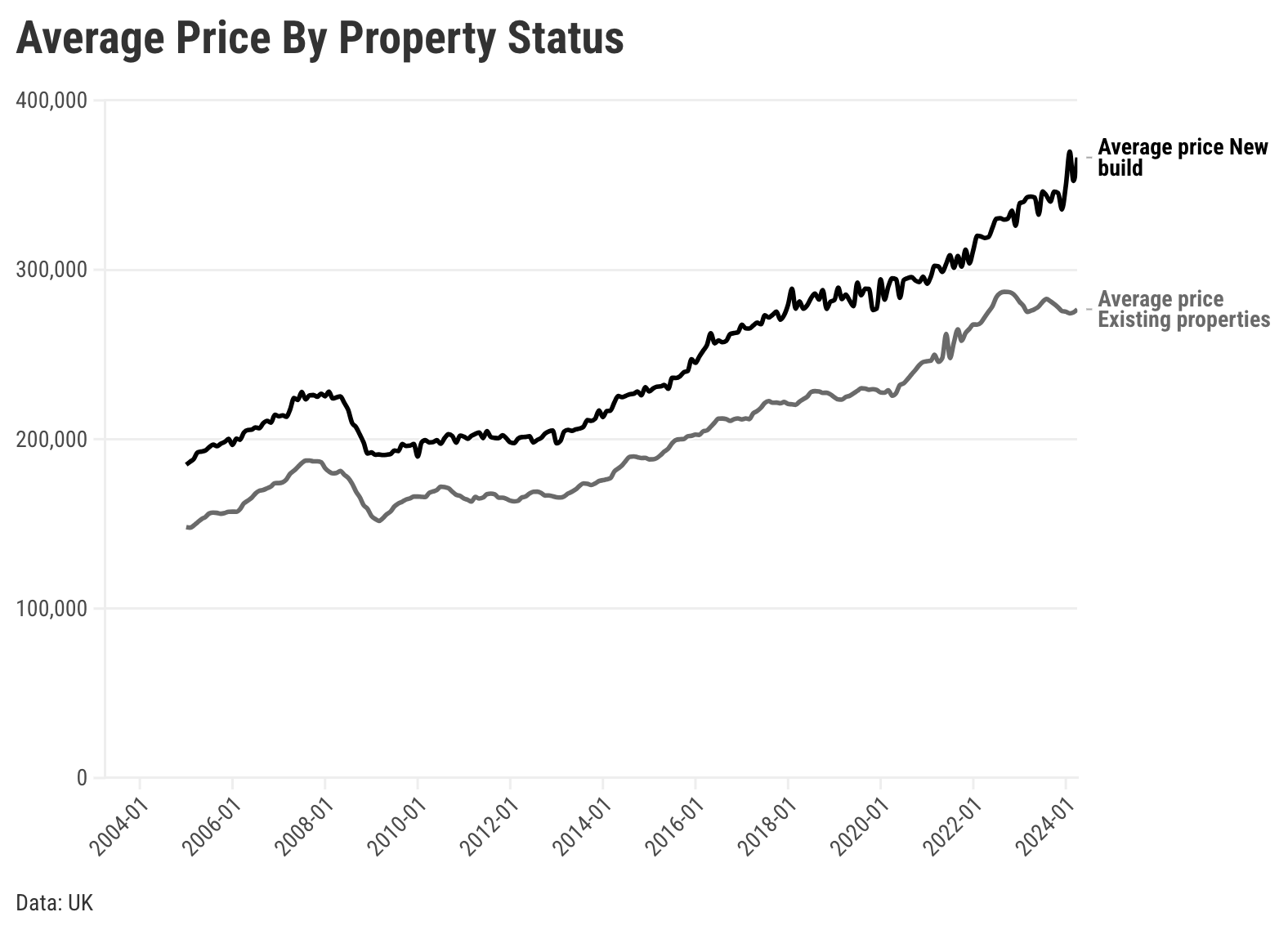

The average new-build home is already 33% more expensive than the average price of an existing property. The maths for building smaller, cheaper homes is much harder to stack up for a private business [7], particularly when other factors, such as the price of materials and planning regulations, are working in the other direction.

For the private sector to be a significant builder of social and affordable housing, there needs to be significant incentives or policy changes. As the CMA highlighted, the private housebuilders build according to market demand, not the wider societal need. When the economy is buoyant, they build, but when it isn’t, they don’t - and, right now, they aren’t [8].

To use some buzzwords of the new Labour Government, this looks like a market failure that needs correcting. Next - the government has revealed the details how it intends to turn things around, so we run through the numbers in the final post of this Housing series.

Worth noting that Scotland abolished the Right to Buy policy in 2016 to preserve its social housing stock.

The amount paid to Persimmon’s Jeff Fairburn was actually revised down from an originally proposed £110m. UK’s biggest housebuilders hand top bosses bumper bonuses, Guardian 2022

The CMA declined to recommend curtailing profits directly because of a) the variability of the wider economic climate, b) they were boosted by low interest rates and Govt. initiatives like ‘Help to Buy’ in the 2010s, and c) some housebuilders still did not perform so well. CMA market study final report into housebuilding, Feb 2024

The area includes England, Scotland and Wales.

The CMA report also found evidence of ‘information-sharing’ of commercially sensitive details (sales prices, incentives and sales rates); issues with private mamangement companies for shared amenities on housing estates; issues with general build quality & customer satisfaction levels; limited innovation and slow adoption of modern building methods. In total, the CMA made 11 recommendations for change which have since been accepted by the Labour Government.

Calculation based on the average house plot size of 150 sqm. The Isle of Wight covers approximately 38,016 hectares.

Estimated costs to build are 85-90% of a private market dwelling, but they often sell at 50-70% of the private market value - HousingForum.org, quoting research by land-valuation start-up, Viability, 2024.

The UK’s biggest housebuilder - Barratt Developments Plc - completed 14,000 homes in the 12 months to June 2024, versus 17000 in the previous period. It predicts even fewer by June 2025. (Full year results, Sept 24)

Reply